This can be a stressful decision, mainly because we have so many choices that are pushed on us each and every day through advertising on the radio, newspaper, billboards, tradeshow...you name it.

So how do you confidently choose the team that will help you with one of the largest purchases you may ever make? If you are lucky enough to have a friend or family member refer you to someone that they have had a positive experience with, then you are already ahead of the game. Its always comforting to have that word of mouth to vouch for someone who is trustworthy, capable and working in your best interest; And the professional that was referred will be very appreciative as well.

I have been in the financial industry for five years, now a mortgage broker for RBC Royal Bank. Before truly understanding RBC's slogan "Advice You Can Bank On", I saw each bank as a generic industry. Do I spend a premium for the Charmin toilet paper or just get the generic brand. Isn't it all the same? Banking is the same, based on what your needs are, "Double Ply or Single Ply".

I am not going to sit here and bad mouth any other financial institution claiming they are the generic, but what is it that separates the quality of a financial institution?

ADVICE!

advice possible with the information I have on hand and collect from interviews with clients that are hoping to achieve the goal of home ownership. We live in a global economy, making the job to forecast and predict mortgage trends very difficult. This is why economists get paid very well, as they are responsible in forecasting and predicting trends based on quality data and strong indicators. Are they always 100% on the mark? No, of course not. Unfortunately they don't have the magic crystal ball that knows all, however, it does give us a direction to move in.

I guess my main motivation for writing this is from a recent experience. I had pre-approved a client for a 5 year fixed rate, as they indicated Fort McMurray was going to be there home for the years to come. Right now, we are living in a time when there is a lot of uncertainty around the cost of funding for credit. So where are rates going? In the short term, it is hard to say. I am not an economist, but I do listen to what is being said, with a lot of focus on the forecast to see the Canada, 5-Year Conventional Mortgage rates increase by the 2nd quarter of 2013 to over 6%. So is now the time to lock yourself into a longer term?

Again it goes back to your goal, which is different for everyone. My warning is when someone is trying to sell you a mortgage on rate alone. I will admit, I have gotten caught up in the excitement before, when RBC put a big sale offer in the market, but I am not here just to sell a rate. I don't want to be the generic brand, I want to the Charmin. And the Charmin comes with "Double Ply = Advice & Solutions".

So back to my motivation for this entry.

My client received a rate of 3.74% for 5 years from me. Decent rate, competitive, and affordable.

Now the client is being swayed over to a competitor with a 2 year fixed rate of 2.49%. I know what your thinking, GREAT RATE! you got to take it. At first I thought the same thing, but something about it bothered me, other than losing the clients business. So I started to run the following calculations.

To keep things relevant to Fort McMurray and simple I will use a purchase price of $500,000.

With an amortization over 30 years and monthly payments.

Mortgage Payment Calculator: https://www.rbcroyalbank.com/cgi-bin/mortgage/mpc/start.cgi

Based on a 5 year fixed rate of 3.74%

Total Payments | Cost of Borrowing | |

Monthly Payments | over 5 years | Over 5 years |

| Principle & Interest | Principle & Interest | Interest Only |

| $ 2,304.59 | $ 138,275.40 | $ 88,369.46 |

Total Principle Paid over 5 years | $ 49,905.94 | |

Total Principle remaining after 5 years | $ 450,094.06 | |

Based on a 2 year fixed rate of 2.49%

Total Payments | Cost of Borrowing | |

Monthly Payments | over 2 years | Over 2 years |

| Principle & Interest | Principle & Interest | Interest Only |

| $ 1,969.68 | $ 47,272.32 | $ 24,229.48 |

Total Principle Paid over 2 years | $ 23,042.84 | |

Total Principle remaining after 2 years | $ 476,957.16 | |

So where is the downside? Your payments are $334.91 less per month.

Sit down cause this is were the advice portion comes in. Going back and understanding that the client is planning on living in this home longer than 2 years I would advise to lock in for a longer term. The competitor is aware of all the same market conditions and forecasts that I am. So why offer a great rate, if rates are going up? Won't they lose money? In the short run of two years, probably, but there is a plan to their madness. Psychologically, when its time to renew our mortgage, we don't typically put the same effort into shopping around again, as we don't want to apply and go through the credit checks and produce documents like we had to the first time. So typically we just choose a new term with our current lender, cause its easy.

By the renewal date the forecast for the Canada, 5-Year Conventional Mortgage rate is predicted to be around 6.79% - 6.99%, based on forecast statistics by The Conference Board of Canada. http://www.conferenceboard.ca/

In order to break even, you would have to achieve a rate of 4.62% for the remaining 3 years to match the 3.74% for 5 years.

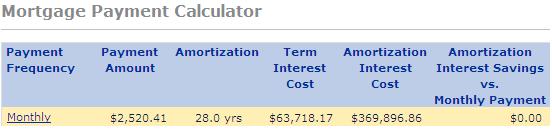

Based on a 3 year fixed rate of 4.62%

Total Payments | Cost of Borrowing | |

Monthly Payments | over 3 years | Over 3 years |

| Principle & Interest | Principle & Interest | Interest Only |

| $ 2,520.41 | $ 90,734.76 | $ 63,718.17 |

Total Principle Paid over 3 years | $ 27,016.59 | |

Total Principle remaining after 3 years | $ 449,940.57 | |

In the first 2 years of your mortgage term you would have paid $334.91 less per month = $8037.84

In the last 3 years of the mortgage term you would have paid $215.85 more per month = $7769.52, if you are able to obtain a rate of 4.62% at the time of your renewal.

Do I know 100% rate will be going up as forecasted? No, but I am using the data and indicators we have today to make an educated decision and provide the best advice possible for my clients.

In the end you have to make the choice.

Run this race like the Hare and take the risk of higher rates before reaching the end.

or

Take the slow and steady pace like the Tortoise for a strong finish despite rate changes.

Please leave any comments as I would love to know your thought around this topic.

Cheer,

Eric Dunham

RBC Mortgage Specialist